AI coding agent startup Niteshift has raised a $7 million seed round led by Greylock’s Jerry Chen. That’s a modest sum by AI standards, but the startup, founded by two former early Datadog engineers, has attracted some big-name angels like Reid Hoffman, Datadog’s Olivier Pomel and Alexis Lê-Quôc, Ankur Goyal of Braintrust, and Misha Laskin of Reflection AI.

Founded by Sajid Mehmood and Conor Branagan, who helped grow Datadog from its early days to a multi-billion valuation, the company has entered the crowded AI coding space with a compelling idea: Why would any company trust its most sensitive assets — code that runs its products — directly to model makers like OpenAI and Anthropic, given that those companies are constantly “killing” startups and businesses by launching competing apps?

Mehmood, who is CEO, likens it to Datadog’s early growth, when the monitoring company won e-commerce customers who refused to build on Amazon Web Services. It was a reasonable concern, given that Amazon was simultaneously putting many of those same retail stores out of business in what became known as the “retail apocalypse.”

The AI equivalent, as Mehmood sees it, is already underway. Anthropic, OpenAI, and others are moving fast into vertical software markets — what some are calling the SaaSpocalypse.

“At Datadog we saw this clearly,” Mehmood said. “A big part of our multicloud business came from e-commerce businesses who did not want to run on Amazon, right? … We are absolutely going to see the same dynamic as Anthropic goes to compete in legal and healthcare and finance and whatever else.”

The bet is that companies will increasingly seek infrastructure that separates the coding model from all the other orchestration needed to ensure AI-generated code is properly vetted and maintained (and that they’ll want a vendor without a competing agenda).

To be clear, Niteshift isn’t replacing Claude Code or Codex, the two most popular coding agents. It argues that it reduces dependence on them.

Niteshift’s AI coding cloud will route between those models — along with open source options and others — based on the needs of each project.

“Being able to switch between GPT and cloud models is important,” Mehmood said, “Everybody’s worried about getting stepped on by these giants.”

That idea is what got Greylock’s Chen to bite.

“As the frontier labs move up the stack, there’s an opportunity to offer customers an alternate path: unbundling their agents from the infrastructure they run on,” Chen told TechCrunch. “Niteshift is building the platform that enables this for coding agents, letting customers invest deeply in their developer tooling without locking themselves into a single model or agent vendor.”

More than that, Niteshift isn’t selling tokens. It sells infrastructure, charging like a cloud provider, with per-minute usage rates.

“Everybody else is selling labor replacement intelligence,” Mehmood said. “We’re selling software to agents, as opposed to humans — but we’re still out here selling software.”

Even so, Niteshift is entering a crowded market of AI coding tools. Model independence isn’t a novel idea, and Niteshift’s competitors have a massive head start. That includes Cursor, though it could soon be gobbled up by SpaceX; Cognition, which just raised $1 billion at a $26 billion valuation; Amazon Bedrock; and AI gateway platform OpenRouter, which just raised $113 million at a $1.3 billion valuation. The list goes on.

Mehmood’s answer to all of that is the founding team’s depth. Mehmood and Branagan didn’t just study these problems — they lived them, scaling Datadog through the exact growing pains that large engineering organizations now face with AI-generated code. Teams, he said, need to run, test, and verify software autonomously in their real production environments, and they need infrastructure built by people who’ve done it at scale.

The three hard-tech moonshots fueling SpaceX’s unbelievable IPO

SpaceX is coming to market on Friday, and investors can barely contain their excitement. The $75 billion stock offering is reportedly deeply over-subscribed, with some institutional investors ponying up for $10 billion blocks of Elon Musk’s empire.

There are lots of reasons to be skeptical of the investment — big IPOs tend to sink, the company is losing money, and Musk’s erratic online behavior would be terrifying coming from any other tech CEO — but it doesn’t seem to be slowing anyone down. Tech investors have learned to never bet against Elon, whatever the business logic indicates.

But a dispassionate look at SpaceX’s financial plans can still tell us a lot about what they’re betting on: A business centered around orbital data centers that emerged in the last 18 months as Musk sought a vision that would unite his conglomerate ahead of its IPO.

In true Musk style, it’s a bold scheme, and one that requires at least three near-impossible feats of engineering: a reusable rocket, a brand-new American chip foundry, and a sprint to build satellites faster than ever before.

That kind of business plan can be difficult to score. This week, two analyses tried to offer a more a sober assessment of SpaceX’s plan — one from Morningstar, the financial research firm, and another from Aswath Damodaran, a New York University finance professor who takes a special interest in corporate valuation. Both exercises find SpaceX significantly less valuable than the nearly $1.8 trillion assessment proffered by the company’s bankers. Morningstar assigns a value of about $825 billion, while Damodaran suggests the company is worth $1.2 trillion.

The significant difference is, in many ways, the result of bolting a world-beating space monopoly to a far riskier AI business. Morningstar’s analyst characterizes the difference between their assessment of a fair value of $63 a share, and SpaceX’s offering price of $135, as a $72 call option on the company’s ability to deliver orbital data centers at the rate and capability that Musk believes is possible.

In both analyses, the high margins of the company’s space launch business and its satellite internet network are the most attractive things about the company, while its AI business is the most uncertain.

To cloud or not to cloud?

Part of the question is, what is SpaceX’s AI business? In the company’s S-1 market analysis, it frames its largest opportunity in enterprise AI — that its models will power coding tools built by the team it acqui-hired from Cursor, or the company’s Macrohard project, which is intended to equip digital agents with the capabilities to perform white-collar labor. SpaceX assessed the total market for that business as $22.7 trillion, compared to $2.4 trillion for AI infrastructure and just under $2 trillion for the company’s space efforts.

But that contradicts the company’s recent deals to sell significant amounts of compute to Anthropic and Google, ostensible competitors in the model business. That’s not out of place for a Musk company; SpaceX frequently launches satellites operated by competitors to its Starlink network. It just usually does that from a place of strength, not while playing catch-up.

Acting like a neocloud might be good near-term business, but it raises the question of where value will accrue in the AI tech stack: Is it better to be a compute provider or a model-builder, if you can’t be both?

The scaling logic that dominates the AI business demands that serious frontier labs constantly train new and more powerful models (or, as Musk admitted in his recent lawsuit against Sam Altman, by distilling capabilities from other companies’ models). Any competitor not rushing ahead is likely to fall behind, although the rising abilities of cheaper open source models might undermine that dynamic.

Space data centers are one way to square the circle, providing so much compute that SpaceX could effectively do both.

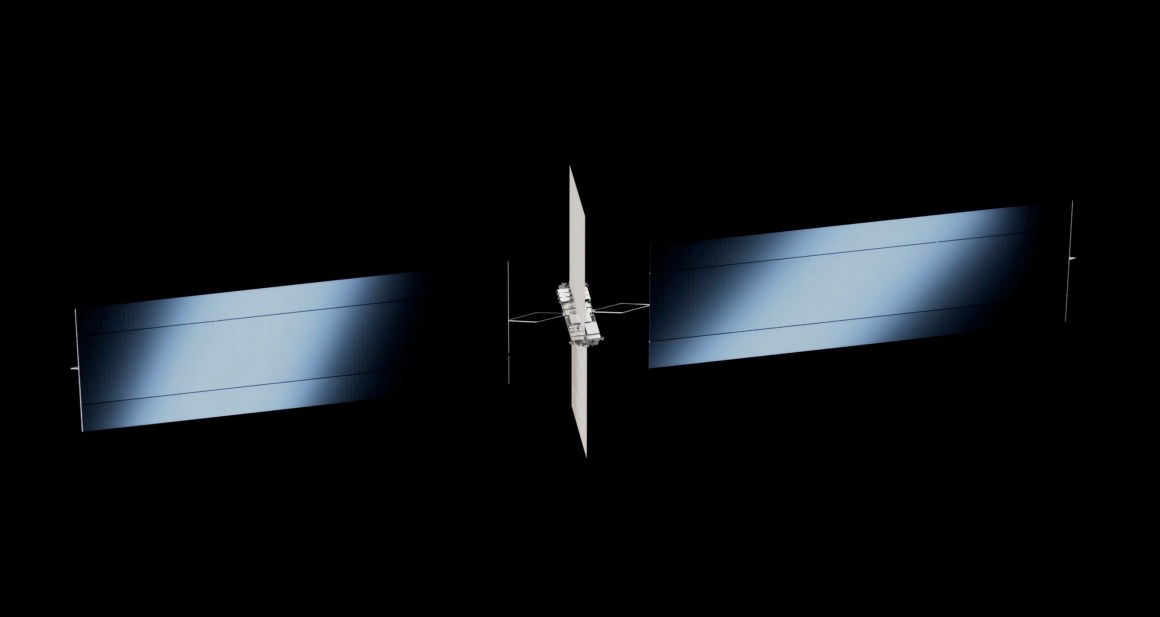

Musk’s space data center architecture

In a video interview released by SpaceX this week, Musk laid out the logic for why SpaceX is best positioned to deliver on data centers. The core of the argument was that SpaceX is the only company capable of putting a lot of mass on orbit cheaply, building a lot of solar panels, and building a lot of chips. In general, industry experts see space data centers at scale being about a decade away, but Musk argued (with a lot of caveats) that they are much closer.

“This is not a promise of what we’ll do,” Musk said in the video. “This is what we are going to try to do, and think we probably can do, which is to get to roughly an annualized rate of a gigawatt per year by the end of next year, in terms of space AI compute.”

Based on his expected maximum power delivery of 150 kW per satellite, that’s a production rate of 6,666 satellites a year, or about 556 a month. That’s roughly twice the reported current production rate of Starlink satellites, which is just 70 a week. Though Musk says that the AI satellites are simpler in architecture, that’s a lot to ask for a production facility that hasn’t been built yet. The company is also still building out its solar panel production facility.

That’s before we get to Terafab, the company’s much-discussed chip foundry, which Musk sees feeding into the later stages of this product as the company tries to scale up to a terawatt of annual compute production. Chip fabs are some of the hardest modern industrial projects, typically costing billions of dollars and taking as long as a decade to build.

Then there’s the most vital question: What about Starship, the key to SpaceX’s ability to economically put all those chips in orbit?

A recent test flight went well enough, but it didn’t suggest that rapid reusability is right around the corner. SpaceX may end up reusing just the booster at first, which would raise the costs of the space data center roll-out. For now, the company is still undergoing a mishap investigation for the FAA to understand why the booster stage failed to make a controlled reentry as planned. SpaceX hasn’t responded to questions about when the vehicle will fly again, thought it has said it expects to begin launching Starlink satellites with it by the end of this year.

But take that with a grain of salt: Consider that NASA, which has a nearly $4 billion contract with SpaceX to use Starship as a moon lander, still isn’t ready to commit to a test mission with the vehicle scheduled for late 2027.

Buyer Beware

As public investors get their hands on SpaceX shares, they’ll find themselves owning a near-monopoly on access to space in the U.S. and Europe, a world-spanning communications network, and a wager on the most ambitious infrastructure project of the AI era.

Those projects depend on SpaceX creating something never seen before — a fully reusable rocket. The company will also need to build a high-rate production facility for AI satellites, but do so in 18 months, not the decade it took to develop its Starlink manufacturing. Finally, it will need to build a chip foundry in the U.S., something even dedicated silicon firms are reluctant to take on. Musk is right that SpaceX is the only company positioned to build any of this anytime soon, but that speaks to the magnitude of the challenge as much as the company’s likelihood of achieving it.

Musk used to say he wouldn’t take SpaceX public until he reached Mars, since fickle investors might lose faith along the way. Those plans may have been put on hold, but what he’s laid out ahead of the company’s IPO could be just as difficult.